The gold price is on the rise and that is not surprising.

Where leading currencies are falling apart at their seams, global geopolitical uncertainties persist, protectionist policies are in the making and a global recession is becoming increasingly likely, Gold is most certainly one of those solid investment solutions to look at.

The price for gold is now back at over USD 1.300 for the first time since Summer 2018, and has remained fairly steady with demand increasing.

Gold as a safe-haven asset – but who is buying?

First off, central banks have increasingly been adding gold to their portfolios. In fact, they have not been buying gold as much as today since 1971. The World Gold Council (WGC) notes that 651.5 tons of gold reserves have been bought in 2018. A large part of this was acquired by emerging-market central banks in order to diversify their currency reserves away from and reduce their exposure to the USD such as China, India and Azerbaijan.

Exchange-traded funds, which are the most favoured means of investors to buy gold, are starting to rise as well though still not concurrent with the major highs six, seven years ago.

Retail investment in gold has remained steadily on an upward trend rising by 4% last year according to the WGC. Following the Global Financial Crisis (GFC), private investors have been moving their funds into safer assets with potentially less return but a higher safety margin. The mindset not only of the investors that burnt their fingers during the GFC but particularly the younger generation (the Millennials) have become a lot less risk-savvy and are looking for more conservative investments and longer-term solutions.

Gold is increasingly becoming a valuable strategic asset for investors as a source of return, due to its low correlation to major asset classes in both expansionary and recessionary periods, as a mainstream asset that is just as liquid as other financial securities and thanks to its history of improved portfolio risk-adjusted returns.

2019: Bull or Bear?

These variables could well be signalling that 2019 will be a bullish one.

- Financial market instability: marked by expensive valuations and higher market volatility (VIX jumped from 13 in Q3 of 2018 to 21 in Q4 of 2018), on-going and worsening political and economic instability in Europe, potentially higher inflation from protectionist policies and the increased likelihood of a global recession.

- Impact of Rates on the Dollar: there are reasons to believe that the USD is losing steam and will diminish further if the Fed takes a more neutral stand.

- Structural Economic Reforms: emerging markets will play a vital role in the long-term performance of gold. China’s Belt and Road Initiative and India’s active modernization of its economy, the reduction of barriers to commerce and the promoting of fiscal compliance are examples of such reforms.

What the figures show:

The above chart shows the price development of gold over the last 10 years and when it reached its historic high in 2011 at USD 1.920 an ounce.

Two things are apparent in this graph, namely the major lows since the bear market low late 2015 / early 2016 (at USD 1.050 / oz) have been higher than the subsequent last which could well be interpreted as a sign for a stronger market.

There is resistance in the market for the price of gold to reach above the USD 1.360-1.380 level for nearly the last 5 years. Experts argue that this level will be the defining level of whether 2019 will turn into a bullish one. So, we are either looking at typical annual fluctuations or a multi-year bull market once the price of gold exceeds the USD 1.420 – 1.450 level. Should gold exceed this level, then a price development of USD 1.520 could be possible according to Money Week’s Dominic Frisby.

Goldman Sachs shares this opinion. Its head of commodities research, Jeff Currie, said that “gold will hit six-year highs this year. $1.450 is the target – some 10% higher than where we are today.”

Gold is an emotional metal, and sentiment a major driver of price. In the near-term though, the price of gold will be heavily influenced by perception of risk, direction of the USD and FED as well as the impact of structural reforms.

Looking in the more long-term direction, gold will be especially supported by emerging markets (which make up some 70% of the demand for gold consumption) and their developing middle class, its role as an asset of last resort and its ever-expanding use in technology.

Tale or Truth?

Whilst everyone is eyeing gold, SILVER deserves a closer look.

At the end of last year Silver sat sluggish at its lowest level since almost 3 years ago, down 15%. With silver being a hybrid metal – part investment but also exclusively used worldwide in an increasing amount of industrial applications, it is worth looking at the possibility that it may become a leader in 2019.

65% of silver demand is used in industrial applications – solar energy and electrical applications. Key drivers will be rising global manufacturing and industrial production. With a shift towards a more sustainable environment, the demand is likely to increase. As with gold, silver will also remain influenced by inflationary pressures, rising fiscal spending and a tighter labour market.

It is also worth looking at the Gold/Silver Ratio which currently stands at around 84,00-85,00, thence not far off from its peak at 86,39 in November 2018 – the cheapest point since 1995. According to Johann Wiebe, lead metals analyst on the GFMS team at Refinitiv, ʺsilver at present would be a good investmentʺ. Peter Spina, president and chief executive officer of gold and silver news and information provider GoldSeek.com, adds though ʺthat investors should look at silver with at least a one- or two-year investment horizonʺ.

If the world comes to a next financial crisis, Silver will be another safe-asset investment.

We provide services for high-security storage facilities for all precious metals and services for the trade (sell and re-buy) of precious metals as well.

Important warning: Prices of the past do not necessarily repeat in future. Technical analyses may not be correct or even fail under unexpected influential developments in global and national politics, crises, economic developments, natural occurrences etc.

Do only consider to invest funds that you do not need for your current lifestyle or to cover your liabilities!

Palladium outperformed all typical investment products during the last 12 months, a trend continuing since February 2009. Based on the figures from yesterday (13 Feb 2019), palladium gained 42,89% during the last 12 months, and 58,73% during the last 6 months. The price of palladium surpassed the price of gold for the first time since 2001. The gain of palladium during the last 10 years is 600%.

About palladium as an investment class

Palladium is a very scarce precious metal. The annual production is around 210 – 220 metric tons (“mt”; US Geological Survey). Palladium is only mined as a small portion of polymetallic ores. Thus, a specific targeting to substantially increase palladium extraction is not possible.

The largest palladium producers are Russia (81 mt), South Africa (78 mt), Canada (19 mt), Zimbabwe (12 mt) and the USA (13 mt), accounting for 203 mt of the global production (all figures for 2017).

The largest known reserves are in South Africa.

Mine closures at the end of 2017 and the beginning of 2018 led to a decrease of production in 2018. Experts expect a further decrease of production by 2% in 2019, says Metal Focus, London. Analysts do not see a possible supply relief anytime in near future.

About 80% of the global palladium production is used in catalytic converters of petrol cars. Tightening of governmental regulations to reduce the output of particle pollution is increasing the production of petrol cars, compared with diesel cars.

The development of electric cars is well going ahead. But electric cars are not expected to reach a level where they could substantially start replacing cars with conventional fueling, for the next five years.

The palladium market is highly volatile, as seen on the above graphic. It seems to be more predictable than other metals, though, due to the fact that about 80% of the world production is consumed by one single industry, the car industry.

However, there is a huge paper palladium market (contracts based on palladium, futures, options etc.) , mainly serving the purposes of advanturers. There are only 42.000 ozs of palladium on the COMEX vaults, but 2,8 million ozs digital obligations.

The below table with a comparison of the main and m

Palladium compared with other investment products

ost common investment products shows the value changes for 12, 6 and 3 months.

The price development of palladium did surpass all other investment products. While palladium gained 41,89% during the last 12 months (as per yesterday), the next highest investment product is Nasdaq 100 with 7,57%, closely followed by gold on Euro (XAUEUR) with 7,49%, and the Dollar Index with 7,06%. The difference between the Dollar Index on the left and right table stems from the little time gap between saving the left and the right table.

Is it too late to invest in palladium?

We do not provide any investment advices of whatever kind. However, as the market situation and the expectation of market experts show, there seem to be still room for substantial gains.

We do provide services for high-security storage facilities for palladium and services for the trade (sell and re-buy) of palladium as well.

Important warning: Prices of the past do not necessarily repeat in future. Technical analyses may not be correct or even fail under unexpected influential developments in global and national politics, crises, economic developments, natural occurrences etc.

Do only consider to invest funds that you do not need for your current life style or to cover your liabilities!

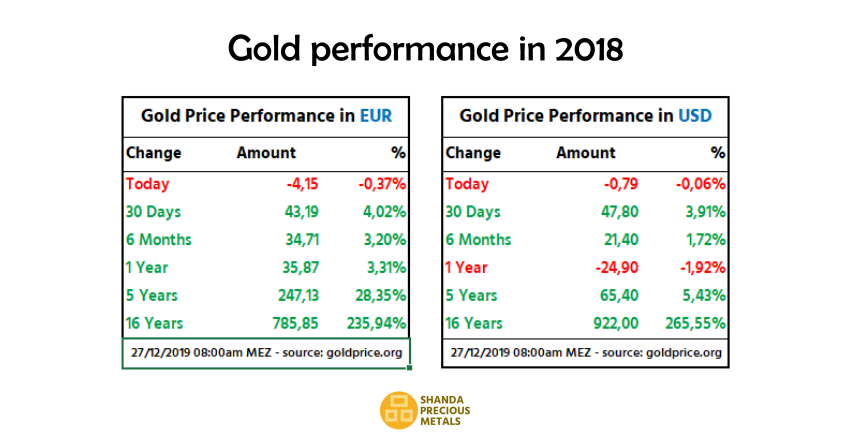

We are watching an extraordinary performance of gold in USD and EUR since 5 months, of 3 months respectively. Gold its on its way to test the 1.300 USD and the 1.200 EUR benchmarks.

The global gold spot price in USD is hiking since 17 August 2018, from 1.172,92 USD/oz to currently 1.275,23 USD/oz today (27 December 2018).

The global gold spot price in USD gained 102,31 USD in 132 days, or 8,72%, resulting in a theoretical annual gain of 24,11%.

Gold denominated in Euro performed even better. The global gold spot price in EUR is increasing since 28 September 2018, from 1.016,151 EUR/oz to currently 1.115,984 EUR/oz today (27 December 2018).

The global gold spot price in EUR gained 99,833 in 90 days, or 8,825%, resulting in a theoretical annual gain of 36,79%.

The sharpest increases could be seen during this December, as the below charts show.

Gold/USD seems to test the 1.300 benchmark, while Gold/EUR tests the 1.200 benchmark, which it already surpassed during the trading hours yesterday and today.

What would happened if I invested in gold x days/months/years ago?

While gold based on USD has had its little flaws in between, it well preserved value in general and thus protected wealth.

Gold based on EUR gained during all terms listed above, except today. While gold in USD just preserved its value in the 5-years term, with a gain of 5,43% (annually 1,09%), gold in EUR gained 28,35% (annually 5,67%).

Thus, gold based on USD and especially gold based on EUR well served the expectations of HNWIs and UHNWIs, who aim to protect their assets from inflation, political decisions and similar risks.

Important warning: Prices of the past do not necessarily repeat in future. Technical analyses may not be correct or even fail under unexpected influential developments in global and national politics, crises, economic developments, natural occurrences etc.

Do only consider investing funds that you do not need for your current life style or to cover your liabilities!

What is the “gold premium” added to the gold spot price?

New gold investors are often wondering about the premium added to the gold spot price. Here you find detailed information about the top-up gold premiums and by what factors they are influenced.

The global gold spot market, like many other markets, is always open, except during the weekends. When the European markets start in the morning, the Asian markets are almost closing, and when the European markets come to an end in the afternoon, the US market opens, and so on. The market price of gold, as of any other commodity or goods, is mainly determined by supply and demand. These markets are called gold spot markets.

As global supply and demand continues 24 hours, except weekends, the gold price changes continuously, depending on the supply and demand of each geographical market.

The supply mainly consists of sales of gold owners such as investors, funds, central banks, insurance companies, private investors etc. Gold supply from production of refineries and scrap smelters plays a relatively small role. The production figures of mines, refineries and scrap smelters are rather a source of speculation than having a determining influence on the market.

The global spot market price of gold can be found online and live, provided by many sources. You will also find the global spot market price of gold on our website.

It is very important to understand what the global spot market price of gold stands for. The gold spot market is the market of the material of gold, without being in any specific physical form such as bars of various sizes or coins. The global gold spot market price is mainly used as a price basis for contracts such as gold future contracts or gold option contracts etc., where physical delivery is not the primary goal.

When a buyer wants to buy physical gold, taking delivery, then a so-called bullion premium is added to the gold spot market price. The bullion premium is simply called “premium” in the industry, or sometimes “mark-up” or “top-up”. The word bullion premium is a bit misleading, because it does not only apply to bullions (bars), but to coins as well.

When gold shall be delivered, it obviously needs to be in a physical form, mainly in form of bars but also coins. The production of bars or coins comes at a cost, and other costs like for transports, insurance, handling etc. must be covered as well. And then there is a profit margin of the seller that shall be covered.

All the above cost factors are covered by the premium, that a buyer of physical gold needs to pay to the seller, on top of the global gold spot market price.

Professional investors or buyers who buy gold, or silver, frequently, are often not talking about the gold price, which is determined by the global gold spot market anyway and does not leave any room for bargaining the price of fine gold. Instead, professional gold investors and gold buyers talk about the gold premium of a seller.

Gold spot price + Gold Premium = Gold Sales Price

The global gold spot market price is not the sales price of gold when a buyer buys gold. The sales price is always the global gold spot market price plus the premium.

There are certain rule-of-thumb standards for the premiums of bars of specific weights and for coins of specific provenience. Those premium standards may vary, depending on a number of factors, such as:

- The form and weight offered, such as bars or coins, and the different weights of bars;

- The volume of gold offered or requested;

- The current market supply and demand situation;

- Global and local economic conditions;

- The national market (country) where gold is bought, and

- The sellers’ own objectives.

Gold premiums – the influence of form and weight

Obviously, it costs a mint much more to produce 1.000 gold bars of one gram each than one gold bar of one kilogram. The same goes for the packing, transport and internal handling, banking fees etc.

For example, two or three employees going to the vault, transferring gold from own stocks to customer stocks, storing these customer stocks in boxes, sealing them, taking note of bar and seal numbers and entering them later into the stock software creates the same costs for ten bars of one kg each as for ten bars of 100 g each. But ten bars of one kg and ten bars of 100 g have a different value. Reflecting these costs to the price results in relatively lower premiums for larger bars and higher premiums for smaller bars or coins.

Although gold premiums may vary based on the factors listed above and explained below, there are some standards of gold premiums for general orientation:

Gold bars of 1 kg: 1,5 – 2,5%

Gold bars of 500 g: 2,5% (rarely demanded)

Gold bars of 250, around : 3% (rarely demanded)

Gold bars of 100 g: 3 – 5%

Gold bars of 50 g, around: 5% (rarely demanded)

Gold bars of 31,1 g (1 ounce): 6% (rarely demanded)

Various gold coins (1 ounce): 5 – 8%

These general rule-of-thumb standards may vary as per the quantity offered or demanded, as per the country where gold is bought, and other reasons mentioned above.

Gold premiums – the influence volume of gold offered or requested

The establishment of a gold seller has to cover certain fixed costs such as overhead costs and payment costs, as mentioned above. If those fixed costs can be spread to a larger amount, the seller can be more flexible with his premiums, still covering costs and realising profit.

The seller’s cost to sell and handle gold bars worth EUR 1,5 million are not six times of the costs selling gold bars worth EUR 250.000. Therefore, the premium for a sale of gold bars worth EUR 1,5 million is likely to be lower than for a sale of gold bars worth EUR 250.000.

Gold premiums – the influence market supply and demand

As with all goods, an over supply on the market drops the prices, and a shortage in supply, because of strong demand, increases the prices. When demand is low, compared with supplies, gold sellers may decrease their premiums in order to attract more buyers.

When demand is high, gold sellers may increase their premiums not only for the reason of increased appetite of buyers, but also to reduce their sales, safeguarding their own stocks in order to be able to meet many buyers’ requests, rather than being sold out within a short period and then watching their own empty vaults, waiting until new deliveries arrive.

While writing this article (December 2018), the delivery time of Swiss refineries is up to 6 to 8 weeks, due to the high demand in physical gold. In times of normal demand or low demand, the delivery time of Swiss refineries is typically 2 days to 1 week.

Gold markets, and silver markets as well, are generally calmer during the summer months, leading to a tendency of slightly lower premiums. When market activities pick up again, typically with the begin of the Indian wedding season in September, the increased volatility results in more buying and selling on the market, which is likely to increase premiums as well.

Gold premiums – the influence global and local economic conditions

Global and local (national) economic conditions are not only influencing the price of gold but, naturally, the premiums as well. The influence on the premium does not necessarily need to be in the same direction as the influence on gold prices. There might be a big demand for gold, which may increase the gold prices. But gold prices may reach or pass acceptance levels in a specific country, leading to difficulties for gold sellers in that country to sell. Consequently, the sellers in that country may drop their premiums.

In countries with a high inflation, like Turkey now, an increasing crowd is trusting gold more than fiat savings (money savings), to preserve their wealth, even if gold demand on a global level stagnates.

Global financial crises like the one caused by Lehman Brothers in 2008, demand in gold and silver increases tremendously, which is reflected to increased premiums as well.

Gold premiums – the influence of a sellers’ own objectives

An individual seller’s own objectives may have an influence on the gold premium, as mentioned above. A concern not to run out of inventory may lead to an increase of a seller’s gold premium. Excessive gold stocks may lead to a lower gold premium of a specific seller.

A seller entering a new market may offer discounted gold premiums to attract more potential buyers. The same typically applies when a seller wants to increase its market share, or to beat strategies of competitors.

Please note that the above information regarding gold premiums applies also to the premiums added to the global spot market prices of silver, platinum and palladium, with the exception that the standard rates are different.

Fiziki Altın ve Gümüșe uzun vadeli yatırım: en emniyetli saklama hizmeti, Avrupa’nın kalbinde.

Fiziki altın ve gümüș, yüzyıllardan beri en güvenilen uzun vadeli yatırım aracıdır.

Fiziki kıymetli madenlere yatırım (bașlıca altın, gümüș, platin ve paladyum olmak üzere), enflasyondan korunmak için en önemli yöntemdir. Örneğin; 1910 yılında ABD’de bir galon benzin 10 US cent’ti, yani USD 0,10. Bu rakam, 0,72 ons gümüș’e eșdeğerdi. 104 yıl sonra, yani 2014 yılında, ABD’de bir galon benzin USD 3,61 değerine yükseldi. Fakat bu fiyatın gümüș karșılığı 2014’te yine 0,72 ons’tu.

Ayrıca, bilindiği gibi, birçok ülkenin Merkez Bankaları tonlarca fiziki altın saklamaktadır ki – para birimlerinin olası așırı bir de değer kaybına ya da bașka ekonomik felaketlere karșı en güvenli önlemdir.

Altın ya da gümüșünüzün hukuki sahibi olmak önemlidir

Fiziki altın ya da gümüșe stratejik yatırım yapan kimseler varlıklarını muhtelif risklere karșı korumak ister.

Ancak enflasyon, korunması gereken risklerden sadece bir tanesidir. Örneğin:

- Bankaların kasa dairelerinde saklanan fiziki altınlar ya da son zamanlarda pek rağbet gören “altın hesapları”na kayıtlı altınların hukuki sahibi bankalardır.

Neden?

%99,99 saflığında olan fiziki altın nakit parayla eșit olarak değerlendirilir ve bu yüzden bankaların nakit varlıklarının arasında yeralmakta ve bankaların bilançolarının aktiflerine kayıtlıdır. Bankalar, kasa dairlerinde bulunan ya da altın hesaplarına endekslenmiș altınlarının hukuki sahipliğini müșterilerine devretse, devredilen altınlar bankanın aktiflerinden ve nakit pozisyonlarından çıkar. Bu durumda bankanın nakit pozisyonları azalıp yasal sermaye-nakit paritesi tehlikeye girer ya da yasal asgari oranının altına iner.

Bu yüzden, bankalar fiziki altın satarken sattıkları altının hukuki mülkiyetini müșterisine devretmeyip sadece kendisine ait olan ve kendisinin bilanço aktiflerinde kalan belirli miktardaki altın için müșterisine bir “hak” verir. Yani, bankadan altın satınalan müșteriye kendine ait olan altın üzerine bir hak tanır. Böylece yasal mülkiyet, bankada kalır. Bir krizde iflas eden bir bankadaki “müșteri” altınları da bankanın varlıkları arasında olduğu için müșteri sözde altınlarını kaybeder.

Dolayısıyla temkinli yatırımcının, altınlarının yasal sahibi olacak șekilde altına yatırım yapması tavsiye edilir. Bu da ancak altınları bankaların dıșında saklama hizmeti veren bir kurulușu tercih ederek mümkündür. - Yukarıda anlatılan sebeplerden dolayı bankalar “sattıkları” fiziki altınları müșterisine teslim etmez, çünkü gerçek yasal sahibi bankadır. İleri yıllarda altınlarınızı bașka bir yerde saklamak istediğinizde bu mümkün olmayacaktır.

Bu yüzden uzun vadeli ciddi yatırımcılar, yine altınlarını bankaların dıșında saklama hizmeti veren bir kuruluș nezdinde saklanmasını tercih eder. - Çok büyük bir risk teșkil etmemekle beraber, satınalınan kıymetli madenlerin sigorta durumuna bakmakta fayda var. Kıymetli madenlerin sigortalanması pek masraflıdır, çünkü sigorta primleri yüksektir. Bu yüzden birçok bankanın sakladıkları kıymetli madenler %100 olarak sigortalı değildir.

Bu riske girmek istemeyen yatırımcı dolayısıyla saklama kurulușunun sigortasından kendisine ait olan kıymetli madenlerin ful sigorta kapsamında olduğuna dair bir teyit belgesini talep eder ya da kıymetli madenlerini kendi namına sigortalatırılmasını talep eder.

Shanda Consult, “Shanda Precious Metals” markası altında Lihtenștayn’de en yüksek güvenlik seviyelerinde bulunan özel binada ve banka sistemi dıșında kıymetli madenler saklama hizmetini sunmaktadır.

Yukarıda değinilen konularla ilgili olarak önemli avantajlarımız:

- Lihtenștayn’deki saklama ve depo șirketi banka ya da finansal kurum olmayıp müșterilere ait olan kıymetli madenleri kendi bilançosunda tutmaz. Kıymetli madenlerini bizimle saklanan müșterilerimiz, kıymetli madenlerinin gerçek yasal sahibidir.

- Müșterilerimiz, kıymetli madenlerini her zaman görebilir, teslim alabilir ya da bașka bir yere nakledilmesini talep edebilir.

- Bizimle saklanan kıymetli madenlerin ful kapsamlı sigortalandığına dair, sigorta tarafından tanzim edilen sigorta teyit belgesi müșterilerimize teslim edilir. Sigorta teyit belgesi müșteri adına tanzim edilir, sigortalı kıymetli madenleri gösterir ve parasal sigorta kapsamını teyit eder.

Fiziki kıymetli maden müșterimizin yatırımları genellikle EUR 200.000’den bașlamasına rağmen daha küçük yatırım planlayan müșteriler de kabul ederiz.

Daha fazla bilgi için așağıdaki formla bize hemen ulașabilirsiniz.

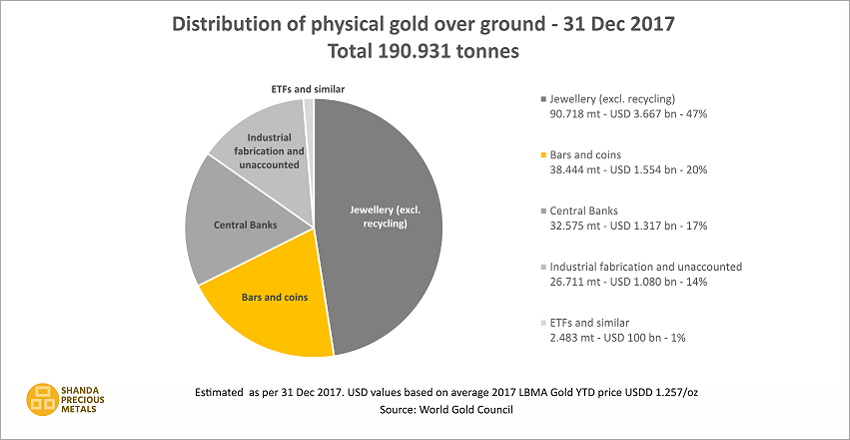

How much gold is there in the world?

The estimated amount of gold over ground existing in the world is 190.931 tonnes, while the estimated amount of gold reserves and resources (gold under ground, unmined) is estimated at 54.000 tonnes.

Physical gold in the world

Physical gold over ground, which means physical gold that has been mined until today, is divided in different market segments.

The largest market segment is physical gold in form of jewellery, amounting to 47% of the existing physical gold in the world, almost the half of all gold. Among the demand-driven price-making market factors, gold in form of jewellery plays the most important role. This can often be seen during the end of the summer season, which is the main wedding season in India.

The second largest market segment is physical gold in form of bars and coins in the hands of the private sector, consisting of natural and legal persons. Natural and legal persons invest in physical gold mainly with the purpose of securing wealth, hedging against various risks and accumulating savings.

Gold bars in the hand of central banks represents only 17% of the entire physical gold over ground in the world, but it can have an impact on global gold prices. That is because when central banks buy or sell gold, they do it often in larger amounts.

A good part of physical gold goes to the industry for various technical applications, including mobile phones. For statistical reasons, unaccounted gold is included in this segment.

Exchange-traded funds, shortly EFTs, and similar products that are based on gold account for only 1% of the physical gold over ground in the world. Thus, they play a minor role among the demand-driven price-making market factors.

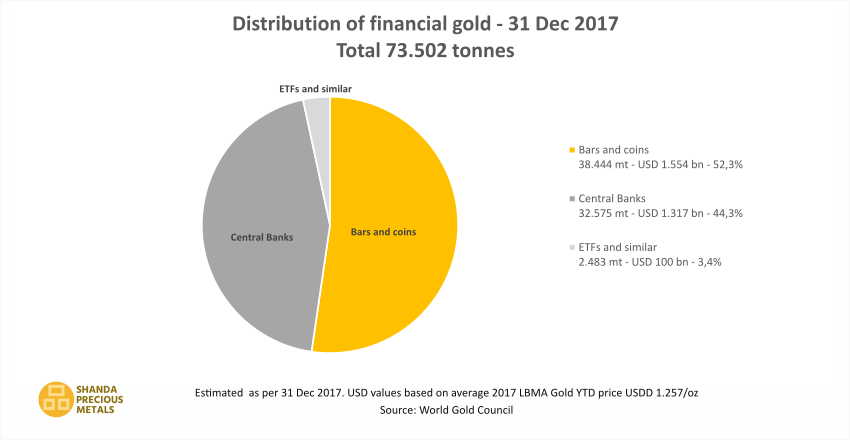

Financial gold

Financial gold is physical gold of the combined market segments gold bars and coins, Central Banks and EFTs. Physical gold of these market segments is called financial gold because they are traded frequently and treated equally to cash.

As seen on the above chart, the total of financial gold was estimated at 73.502 tonnes at the end of 2017 or 38% of all mined physical gold existing in the world.

Gold bars and coins amount to 52,3% of the entire financial gold in the world, thus being an influential factor in the price-finding of the demand-driven gold market.

Gold in the hand of central banks, usually in the form of gold bars, accounts for 44,3% of the financial gold. However, as central banks do not frequently buy or sell gold, this segment plays a relatively small role in the price-finding demand-driven price-finding gold market.

Last but not least, EFTs account for only 3,4% of the financial gold, with naturally little influence by demand.

Under its brand Shanda Precious Metals, Shanda Consults provides services regarding security storage and trade of precious metals such as gold, silver, platinum and palladium. If you like to know more about our services and what makes them outstanding compared with many others, please contact us through below form.